Combating the Trade-off between Sustainability and Economic Stability

06 January 2023•

%2Fuploads%2Finnovations-international-trade%2Farticles%2Fgreen-trade%2Fchris-leboutillier-TUJud0AWAPI-unsplash.jpg&w=3840&q=75)

Lucidity Insights in partnership with Entrepreneur Middle East and DP World published a Special Report on Innovations in International Trade. The report covers a swathe of topics, reviewing the concept of international trade, it’s history and evolution to present day, the different modalities of trade being utilized, and how large the industry has gotten in the past few decades, driven by free trade and globalization, industrialization, and consumerism. It was also interesting to read about the role international trade plays in the wider global economic engine – and how international trade is both affected by and influential in affecting global supply shortages, inflation and the like. The report also dives deeper into the new trade technologies (Trade Tech) as well as Climate Tech, and how technology is working to make the industry, which drives more than a 1/5th of our global economy, more efficient and sustainable.

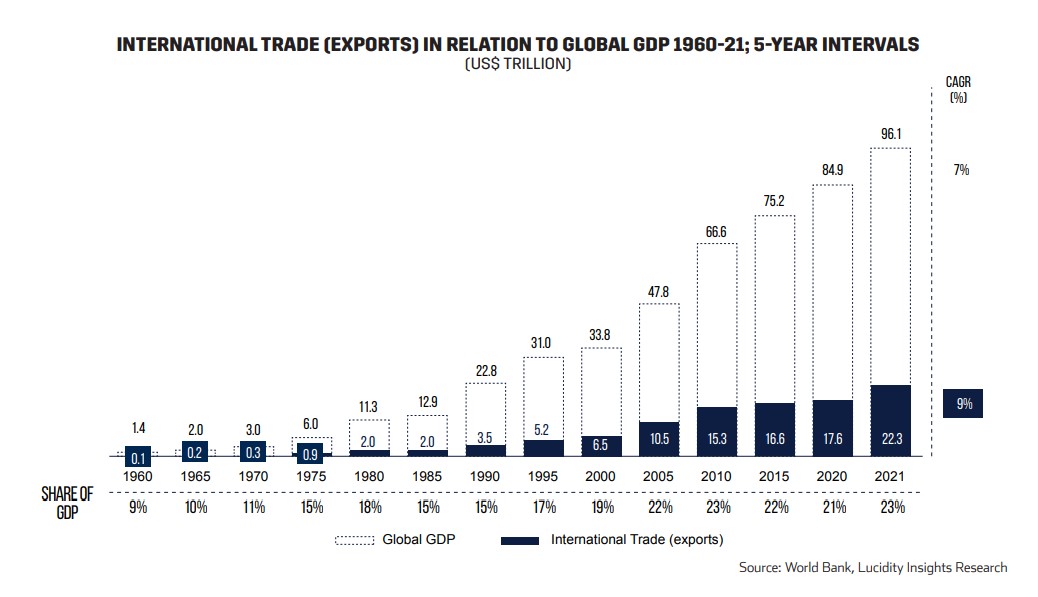

It's amazing to think that more than 46% of our global economy is driven by trade, the import and export of goods around the world. Just looking around my desk can quickly help validate that though. My coffee cup was made in China, but I bought it from a Swedish retailer. The clothes I’m wearing are almost exclusively made in South East Asia. The table I am working on was fabricated in Europe. The ceramic plant pot on my desk was made in Poland. Even the plant itself, a lucky bamboo money tree, is not endemic to the region – though it was likely grown from seed locally. I actually struggle to find something in or around my desk that was made in the Arab world. I settle on a half-empty plastic water bottle from a local distributor which proudly claims it was made here.

What’s more difficult for me to reconcile is that production and trade, the two things that literally determine the world’s economic success (also known as GDP, or gross domestic product) is also contributing negatively and disproportionately to the climate crisis and the sustainability of our ecosystem.

It’s inarguable that since the agricultural revolution gave way to the industrial revolution, the world has witnessed unbelievable economic growth, pulling millions of people out of abject poverty. More people have regular access to electricity, clean drinking water, food on the table, and even greater amounts of disposable income than ever before. I can certainly say my quality of life is greater than that of my grandparents’ generation. Unfortunately, our collective economic growth has also resulted in a significant increase in greenhouse gas emissions (GHG) that are warming the planet each year and contributing to climate change.

It makes perfect logical sense that the wealthier we are, the larger our carbon footprint becomes. We see it time and time again, as we look at the carbon footprints of the world’s wealthiest economies, and compare them with the world’s most impoverished countries. The reality is, as you and I become increasingly wealthy throughout our life, we grow bigger footprints because of the increase in the meat we consume, the cars we drive, the bigger homes we live in (that demand more electricity to light, heat and cool), and the general increase in consumerism we partake in. It’s a bitter-sweet pill to swallow. We work all our young lives to find some level of financial security, and when it comes to celebrate the fact that we are no longer living pay cheque to pay cheque, we now have some level of guilt that the lives we’ve striven for all this time is contributing negatively for the planet.

But what are we to do? That is what the Sustainable Development Goals that the United Nations put out seeks to guide us in. That is why many scientists and futurists are turning to technology to help solve for this big, hairy problem. And investors are getting behind it too. Today, there are nearly 80 Climate Tech unicorns, all working to solve for the over-abundance of GHG emissions in our atmosphere, either by capturing it and recycling GHG emissions in one way or another, or producing products that emit less GHG emissions. For the 18 months between January 2020 and July 2021, US $87.5 billion was invested in ClimateTech startups, and shows no sign of slowing down. You can read more about this and other general sustainability innovations in Lucidity Insights’ latest Special Report titled “Sustainability Innovations and Startups in MENA”.

There is also another up-and-coming industry, specifically looking at tackling the trade sector, called Trade Tech. Trade Tech startups span everything from those that use AI and predictive analytics and robotics to dramatically increase efficiency and reduce processing times of goods traveling the world, all the way to startups that use technology to reduce emissions in the shipping and trade value chain. Many of these Trade Tech startups aim to combat global warming and climate change and hope to become an indispensable tool to achieve carbon-neutrality as early as 2050, with high-tech solutions using advanced AI.

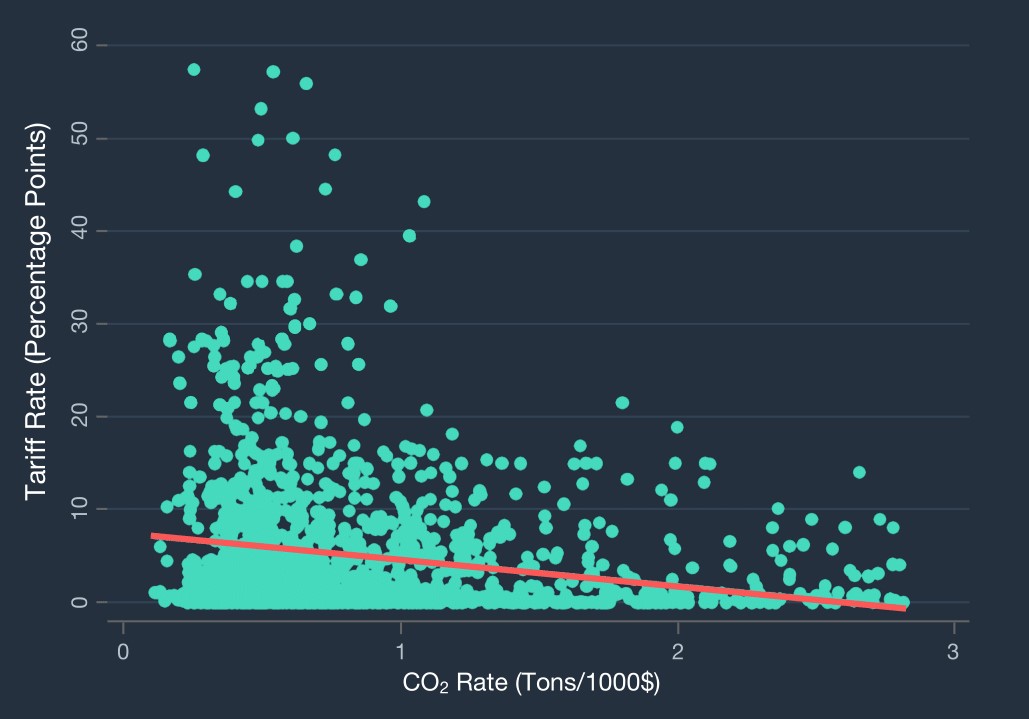

Tariff rates for high VS low emission products

Source: Shapiro, JS. 2020. “The Environmental Bias of Trade Policy.” Quarterly Journal of Economics

Of course, technology is not the only way to combat climate change in trade. Climate conscious policies can certainly help change the rewards of the system. For example, studies carried out by economists in 2020 and 2021 found that energy-intensive goods (read: GHG emission polluting goods) have the lowest tariffs worldwide, creating a trade bias. Economists say no one in their right mind would pay more just to save a little carbon emission when the rest of the world is doing the exact opposite.

It seems, with the significant importance of international trade on our global economy and on our planet, focusing on sustainable levels of production and enabling climate resiliency should be paramount. Policies that will build climate resilience, like lowering tariffs on clean, low-emissions products; such solutions are already underway thanks to groups like Fairtrade and Enhanced Integrated Framework (EIF) whose whole mission and vision is to harness the power of trade to make a better world for farmers, workers, and civilians alike. Last year alone, EIF reported 43 projects targeting gender equity and green trade in collaboration with the UN’s Sustainability Development Goal #13: Climate Action.

The World Trade Organization has also recognized the influence of international trade on green economies with its initiative, Aid for Trade (AFT), promoting climate justice. This year, AFT dove into climate-finance in support of developing countries with trade-related constraints as they are hit hardest by climate-induced crises despite having the lowest greenhouse gas emissions worldwide. Minor climate-related crises can be offset with advanced technologies for water irrigation and conservation as well as crops that, for example, resist high heat and salinity. International trade policies must then remove trade barriers and sanctions to allow these climate-adaptive strategies to be accessible worldwide.

Of course, international trade has also taken a proactive approach towards climate-change prevention through carbon pricing policies. Over 100 countries have considered trade policies such as carbon taxes and emission trading schemes to reduce GHG emissions and many have already been implemented by the International Carbon Action Partnership as of this year.

Though climate change and global warming are international trade challenges felt across the globe, some countries such as the GCC are more vulnerable than others considering their centralized location and extreme temperatures. Luckily for them, however, the UAE and KSA are regional heavy-weights among the top trading countries in the world and may hold the key to climate resilience. The two have pledged net-zero emission targets for 2050 and 2060, respectively, and as the Gulf’s largest economies, the effect that these emission cuts will have will be significant. The UAE will also be hosting the COP28 summit in 2023, which it anticipates will be a major driving factor for making the energy cuts necessary to achieve its zero-carbon goal while inspiring neighboring countries to follow in its newly green footsteps.

%2Fuploads%2Finnovations-international-trade%2Fcover8.jpg&w=3840&q=75)